At a recent presentation before the 10th Annual LeadingAge New York CCRC Summer Summit on the topic of investments in the senior living industry, Patrick Cucinelli, Senior Director of Public Policy Solutions for LeadingAge New York, referred to me as “The best friend of New York’s CCRCs.”

New York’s CCRCs (Continuing Care Retirement Communities) need a friend right now. For the past few years, I have volunteered time to work with a group comprised of CCRC leadership and industry executives who have championed changes to current regulations and worked to educate others on the issues. Our goal is to improve investment conditions for New York’s CCRCs by changing Regulation 140.

CCRCs in New York are at a disadvantage with respect to their investments, which can potentially impact their earning potential and their ability to manage certain investment risks. The ramifications have business implications for these organizations, and more importantly, negatively impact residents in the form of potentially higher fees or reduced access to CCRCs. This affects housing and care affordability and viability for New York’s seniors.

Here’s what you should know about the New York situation:

- Cost of capital is vital to their viability and cost containment. CCRCs raise capital in the debt market to implement strategic initiatives, build new communities or for expansion and capital improvements.

- CCRCs have three primary sources of revenue: Entrance fees paid by residents that add to operating surplus and create their investment pool, monthly residents’ fees and investment returns.

- New York CCRCs report[1] paying a higher interest rate for their debt (in one of the lowest cost of debt environments) than what they can earn on their investments which puts them at a disadvantage.

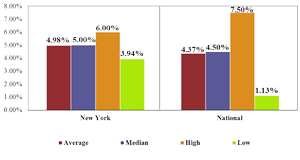

- If a CCRC’s cost of capital is 4.98%, but investment earnings are expected to be 4% or less return (the numbers from our special New York study1), then they are not earning enough to offset the cost of their debt. This creates a negative arbitrage situation. Retaining operating cash is required at certain levels and typically a condition of the lender or bond agreement, so using their low earning cash to pay off the higher cost debt isn’t always an option.

- Communities across the nation are at an advantage relative to New York because they have the potential to earn more from their investments than they are paying for the money they’ve borrowed1. This advantage adds income to their operations and helps to offset expenses, as well as the rate of fee increases for residents.

- The long-term consequences of this situation are potentially higher fees for seniors in New York and a disincentive to build additional CCRCs, resulting in less access and the potential to push costs even higher.

Examples of how the working group would like to resolve Regulation 140’s restrictions that encumber New York’s CCRCs include:

- Allow investment in mutual funds and ETFs without having to apply to a state agency for an exemption. Mutual funds and ETFs offer access to a broad array of asset classes and investment strategies at lower minimums and fees in many cases especially when taking into consideration the internal costs associated with reconciliation and financial oversight tasks. This restriction is inhibiting their ability to access some asset classes on an efficient basis. A more modernized and balanced approach to investing is needed.

- Grant the ability to invest in global bonds or global bond mutual funds or ETFs. This would help diversify portfolios and reduce risks associated with the U.S. interest rate environment.

- Simplify the calculation for the percentage of allowable equities. CCRCs would like the ability to invest up to 35% of their organizations’ surplus assets in equities. Investing a greater portion of their assets in equities can provide a return advantage over time and offer diversification from the fixed income markets.

Our firm conducts an annual senior living survey. In 2014, we issued the third special New York study that help support the work group’s efforts and proposals. This year’s survey1 told us:

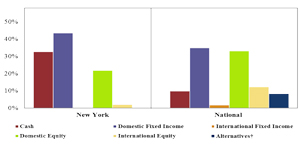

- New York’s CCRCs report holding, on average, 30% more fixed income and cash than communities across the nation.

- Nationally, CCRCs hold on average of 21% more in equities and 8% more in alternatives than New York. Alternative investments are prohibited and the workgroup is not seeking to change this.

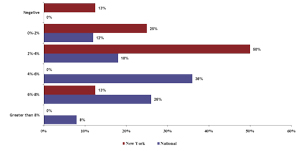

- 88% of New York CCRCs expect a return of 4% or less with 13% expecting a negative return. 70% of CCRCs other than those in New York expect an investment return of 4% or greater.

- The average cost of capital for New York’s CCRCs is 4.98%, among national respondents it’s 4.37%.

Earning more than the cost of capital is not unreasonable and can generally be accomplished without taking extraordinary risks, but New York is hamstrung by investment restrictions. Investment returns are important to the financial health of a CCRC and can help minimize fee increases for residents. While regulators may be focused on risk management, risk isn’t only about being too aggressive; risk can also take the form of being too conservative. The vast majority of CCRCs use an investment consultant1 to help manage their investments providing professional guidance and oversight.

At the Summer Summit, I shared the effect of the current investment restrictions when compared to investing 35% in equities. In a year like 2013, when U.S. equities were up around 30% and fixed income was down -2% for the year, the impact on a $20 million portfolio was -$412,0492. Granted, these returns were unusual compared to long-term averages, but improved diversification and access to investments with greater earning potential are needed for New York CCRCs to outpace their cost of capital and help offset fee increases for their residents.

With minor shifts in the regulations, New York’s CCRCs could move closer to parity with the rest of the nation. The working group will continue to champion changes to Regulation 140 by working closely with the New York Departments of Financial Services and Health.

Stephanie Chedid is the president of Cleary Gull Advisors. Past performance does not guarantee future results and, as with any investment, there is a possibility of loss of principal. Statements made in this blog that reference Cleary Gull Advisors’ 2014 Senior Living Study were based solely on the results of the study and should not be construed as attributable to all senior living organizations in the industry. Cleary Gull Advisors invited 363 senior living organizations from across the nation, including senior living clients of Cleary Gull Advisors, to participate in the study; not every organization that was invited participated in the study. The sample size may not be large enough to produce a statistically meaningful conclusion.

[1] Source: Cleary Gull Advisors 2014 Senior Living Study.